The glut of headlines speculating about UK property can be off-putting. However, the current housing market offers certain advantages that should encourage would-be buyers as we head into 2024.

There’s no doubt that high interest rates have slowed the UK housing market, but that doesn’t mean it’s all doom and gloom for home buyers.

Lower demand for houses means it’s a buyer’s market, so it’s easier to negotiate house prices. Average discounts on the asking price have hit 5.5% according to Zoopla – the highest they have been in 5 years.

Lower purchase prices mean less stamp duty to pay on completion and reduced conveyancing fees and estate agent fees (if you are selling a property to move).

Furthermore, rents are soaring, with Zoopla reporting that average rents for new leases increased by nearly 10% over the past year.

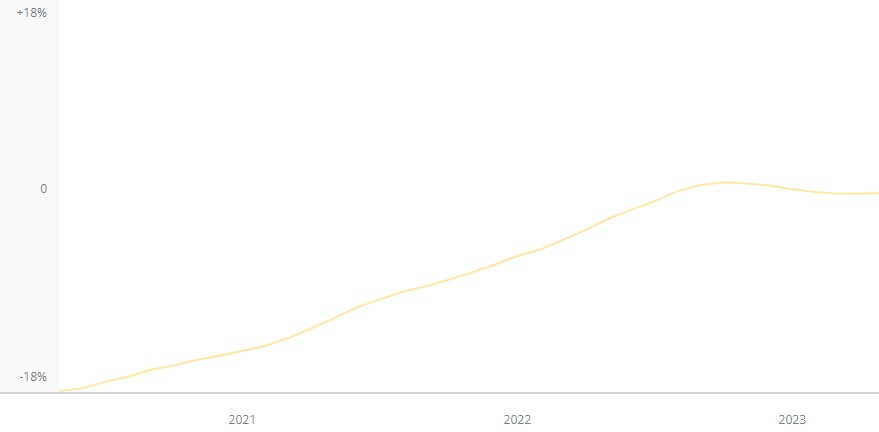

And despite predictions of large falls in house prices, the past year has only seen a modest drop of 1.2%, with the biggest fall taking place at the end of 2022, and prices stabilising and even starting to rise since. This suggests that property remains a stable investment, particularly if you are buying somewhere to live for a substantial period.

Although mortgage rates are high and largely predicted to decrease only slowly, you could go for a tracker mortgage. This will follow the decreasing rates, leaving you gradually better off each month.

Length of Investment

Long term, property is almost always a sound investment – ‘safe as houses’.

Most markets will track upwards over periods of decades, during which time you will have built equity in your house. In that same period, inflation will mean that your monthly payments are worth less, and hopefully increased wages will also make your mortgage payments comparably smaller.

Perhaps most importantly, eventually you will have paid off the mortgage altogether. You then have the security of owning a home outright for you and your family. By this point, you would be unlucky if your home wasn’t worth substantially more than you initially paid for it, even taking into account interest, stamp duty and moving costs.

Short term – if you are looking for somewhere to live for just a few years, the question is often whether it’s better to buy or rent.

Houses are usually seen as a long-term investment, so if you are buying somewhere with a plan to keep it for only a few years, the decision can be more difficult.

Some are saying prices may fall next year – this is always a risk with any investment. However, there are more and more signs that the housing market will recover in 2024, meaning that prices will do the opposite and rise.

If you know you will only be living somewhere for a few years, do some research on the strength of the local market, and the types of houses that sell well and check out recent sale prices to make sure you aren’t overpaying. Don’t go for anything risky or too niche. You might love the wonky thatched cottage in the middle of nowhere, but if you need to sell it quickly, you could struggle.

If the alternative is renting, consider that you are missing an opportunity to build equity with the money you are paying to a mortgage each month, rather than lining your landlord’s pockets.

In addition, as pointed out on Reddit, if you can fix your mortgage at a rate you can manage, this is likely to become easier to pay as your wages increase over time. On the other hand, rental costs tend to follow the market and increase year-on-year.

Location

The most important factor relating to location is whether it is somewhere you want to live! However, if you are investing a substantial amount of money, it pays to dig a bit deeper.

Prices are falling in some locations, and are steady or even rising in others.

According to Hometrack, cities like Nottingham, Birmingham, Sheffield, Leeds and Manchester have all seen above-average growth over the past year.

Similarly, regions around these cities have performed well. August–August data from the Land Registry showed that house prices in High Peak, near Sheffield grew by more than 2%; prices in Derby, near Nottingham, grew by 3% and Cheshire East, inc. towns like Macclesfield, grew by 2.5%.

While house prices did fall from their peak at the end of summer 2022, the prices very quickly stabilised in the 2023 new year. This shows the robustness of the market in these areas and suggests that prices could remain stable or even rise over the coming years.

Other areas, mainly in the South of England, were more affected by the interest rate rises; however, even in cities like Cambridge and London, where we haven’t seen growth, prices have only fallen by 0.2% and 0.5% respectively, over the past 12 months.

With experts predicting we have seen the worst of interest rate rises, these are the areas where you might be able to negotiate more on house price, and get a good deal.

We would say this, but if you are about to part with hundreds of thousands of pounds, it makes sense to get the property surveyed.

Whereas a mortgage valuation will simply check that the amount the bank is investing in the transaction is secure, an RICS Level 2 or RICS Level 3 survey is a detailed inspection looking for any property defects that could affect the property’s value, or be costly to repair and maintain.

Many surveyors, including Allcott Associates, can also provide a market valuation so that you can have an idea of whether your offer is realistic and whether you are getting value for money.

Allcott Associates’ building surveys

Our homebuyer reports and building surveys are some of the most detailed in the industry. They are all produced by experienced surveyors, with photos illustrating our findings throughout.

Check out our reviews on Google and Reviews.co.uk, or view our sample reports.